TL;DR:

- Lender requirements for Japanese Knotweed vary, often needing a survey and insurance-backed guarantee.

- Proactive weed checks during May to September can prevent costly delays and support remortgage success.

- Clear documentation and specialist surveys are vital for lender approval and managing property value impact.

How to clear a weed check for remortgage: 5 key steps

Imagine your remortgage application stalling weeks before completion because a surveyor flagged Japanese Knotweed on your boundary. It happens more often than homeowners expect, and the consequences range from lender retention to outright refusal. Invasive weeds, particularly Japanese Knotweed, are among the most consequential property issues a lender can encounter, yet many homeowners approach the remortgage process without giving them a second thought. This guide walks you through every stage of clearing a weed check, from understanding what your lender actually demands to presenting a compliant outcome that protects your property value and keeps your remortgage on track.

Table of Contents

- Understand lender requirements for weed checks

- Preparing for a successful property weed survey

- Step-by-step: conducting your weed check

- Interpreting results and ensuring lender approval

- The overlooked value of proactive weed checks

- Get expert support for your remortgage weed check

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Check lender policy first | Lender requirements for weed checks and remediation vary, so confirm before starting your remortgage application. |

| Optimal timing for surveys | Schedule your weed survey between May and September for the best chance of accurate detection. |

| Always use qualified surveyors | Choose RICS-compliant professionals familiar with Japanese Knotweed to ensure accurate results and compliance. |

| Prepare documentation in advance | Gather past survey reports and property details early to speed up the remortgage process and avoid delays. |

| Remediation may be required | If invasive weeds are found, robust remediation and insurance-backed guarantees may be needed for lender approval. |

Understand lender requirements for weed checks

Having set the stage for the importance of weed checks, let’s examine lender requirements so you can prepare effectively. The first and most important thing to understand is that mortgage lenders do not share a single, uniform policy on Japanese Knotweed or invasive weeds. Their attitudes range from cautious acceptance to outright refusal, and knowing which camp your chosen lender falls into before you commission any survey is essential.

As lender policies vary considerably, some major high street lenders such as Nationwide and Lloyds take strict positions, applying retentions or refusing to lend entirely where knotweed is identified without a fully documented remediation plan. Barclays, by contrast, is known to accept lending where an insurance-backed guarantee (IBG) is in place. Specialist lenders and bridging finance providers are often the most flexible option for complex cases where remediation is ongoing.

An IBG is a formal guarantee, typically lasting between 5 and 10 years, issued by an approved invasive weed specialist confirming that a treatment or management plan is active and insured. Many mainstream lenders will not proceed without one. Understanding knotweed mortgage checks before you apply can prevent significant delays.

Here is a comparison of typical lender approaches:

| Lender type | Stance on knotweed | What they typically require |

|---|---|---|

| Strict high street lenders | Refusal or significant retention | Full remediation plan and completed IBG |

| Flexible high street lenders | Acceptance with conditions | Active IBG from qualified specialist |

| Specialist lenders | Case-by-case assessment | Remediation plan, surveyor report, IBG |

| Bridging finance providers | Generally flexible | Risk assessment and exit strategy |

Key requirements you should establish before applying include:

- Weed survey report: a formal document produced by a qualified surveyor confirming the presence or absence of invasive species

- Insurance-backed guarantee: mandatory for many lenders where knotweed is confirmed

- Remediation plan: a documented strategy for treatment, typically spanning several years

- Lender-specific documentation thresholds: some lenders require RICS-compliant surveys; others accept specialist assessments

Speaking with a remortgage solicitor early in the process is also advisable, as solicitors can clarify what documentation will be required during conveyancing. Reviewing knotweed mortgage issues in advance ensures you are not blindsided by conditions once your application is in progress. Taking this step before commissioning a survey means you commission exactly the right type of report, from the right type of specialist, to satisfy your specific lender.

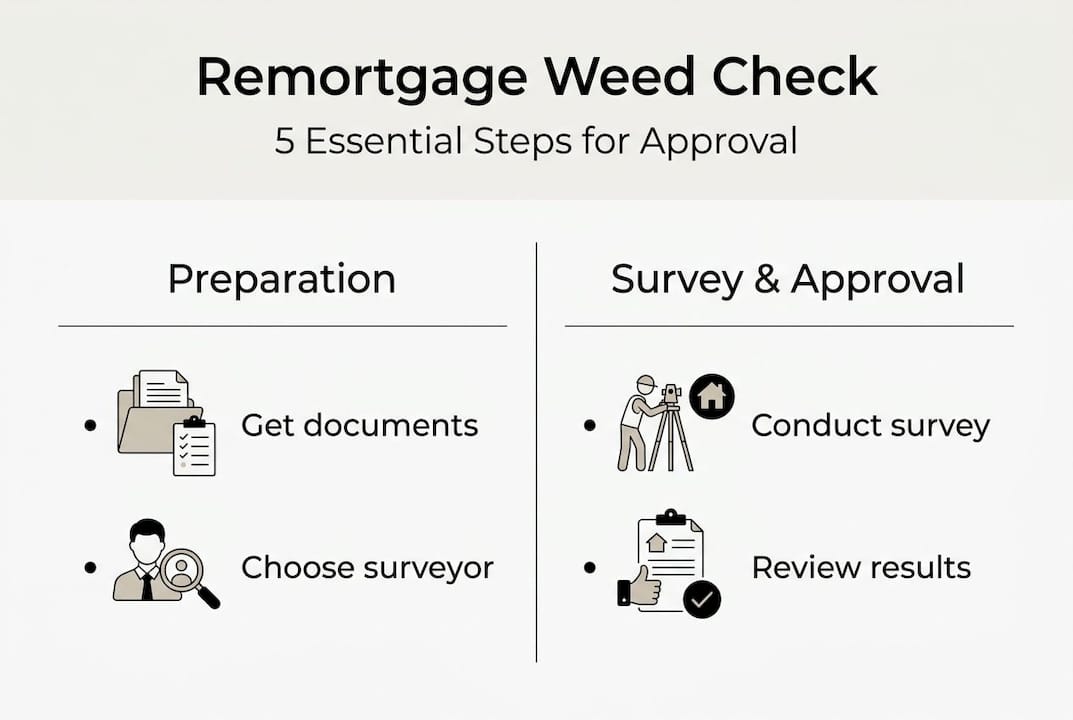

Preparing for a successful property weed survey

Once you understand lender requirements, preparing your property and paperwork for a weed check is the next step. Thorough preparation significantly reduces the risk of a delayed or inconclusive survey outcome, which can cost weeks of remortgage time and, in some cases, the offer itself.

Start by gathering any previous survey documentation held for the property. If a weed survey was carried out during your original purchase, that report will give the incoming surveyor a baseline and may accelerate the assessment process. Prior treatment records, contractor invoices, and any IBG documents already in existence should all be organised and made available before the visit.

Timing matters considerably. As proactive surveys before application can prevent costly delays, booking within the optimal growing season from May to September is strongly recommended. Japanese Knotweed is most visually identifiable during this period, when its distinctive hollow bamboo-like canes, shield-shaped leaves, and small white flowers are visible. Attempting a survey outside this window risks an inconclusive result, which many lenders will not accept.

The table below summarises the key preparation steps and their importance:

| Preparation step | Why it matters |

|---|---|

| Collate previous survey reports | Provides baseline data and historical context |

| Organise treatment and IBG records | Demonstrates proactive management to lender |

| Schedule survey in May to September | Maximises detection accuracy and visual confirmation |

| Select RICS-compliant surveyor with weed expertise | Ensures lender-acceptable documentation |

| Clear site access prior to survey | Prevents delays on the day and missed assessment areas |

When selecting a surveyor, prioritise specialists who are experienced with invasive plant identification alongside RICS compliance. A generalist building surveyor may not possess the specific botanical knowledge to accurately identify early-stage knotweed or distinguish it from similar-looking species such as Russian Vine or Bindweed. Understanding knotweed property value impact is also useful context, as surveyors will factor proximity to structures, spread, and treatment history into their valuation notes.

Before the survey day, walk your own boundaries and garden areas. Note any areas of dense vegetation, recent disturbance, or soil movement, as these can be indicators of rhizome activity beneath the surface. Japanese Knotweed rhizomes can extend up to 3 metres deep and 7 metres laterally, meaning visible surface growth is often just a fraction of the plant’s full extent.

Consulting a conveyancing timeline guide can also help you position the survey correctly within your overall remortgage timetable, ensuring the report is ready when lenders need it without unnecessary waiting periods.

Pro Tip: Book your weed survey at least 6 to 8 weeks before you intend to submit your remortgage application. This leaves sufficient time to address any findings, commission further specialist assessments if required, and obtain documentation without creating pressure on your completion date.

Step-by-step: conducting your weed check

You have prepared your documents and scheduled the right time; here is how the weed check is performed step by step.

- Initial site walkthrough: The surveyor carries out a structured perimeter and garden inspection, examining boundaries, outbuildings, paved areas, and any land adjacent to or bordering the property. They assess soil disturbance, raised paving, and cracked structures that may indicate rhizome pressure from below.

- Identification of invasive species signs: Surveyors look for tell-tale growth patterns, including the distinctive reddish-purple shoots in early spring, the dense bamboo-like cane clusters in summer, and dried hollow canes in autumn and winter. They also check for species such as Giant Hogweed, Himalayan Balsam, and Rhododendron ponticum, all of which are controlled under the Wildlife and Countryside Act 1981.

- Photographic and mapping evidence: Confirmed or suspected invasive species are photographed and plotted onto a site plan. This mapping process is critical for lender reporting, as it demonstrates the precise location of any infestation in relation to the property’s structures, boundary, and neighbouring land.

- RICS protocol documentation: The surveyor completes formal documentation in line with RICS guidance, categorising the infestation, if present, using the recognised 4-point Management Plan category system, ranging from Category 4 (low risk, remote from structures) through to Category 1 (immediate structural threat).

- Report preparation and issue: A formal written report is produced, typically within 5 to 10 working days, detailing findings, risk assessment, and recommended remediation actions where applicable.

As May to September remains the optimal detection window, scheduling outside this period may produce an inconclusive report. Surveyors working in winter often note “not assessed” against certain areas, which can be problematic for lender compliance.

Common mistakes to avoid:

- Failing to clear vegetation or debris from boundary areas before the surveyor arrives

- Booking the survey in late autumn or winter when growth is not visible

- Using a surveyor without specialist invasive plant identification training

- Not disclosing previous knotweed history to the surveyor before the assessment

Thorough preparation before a weed survey is not a formality. It is the single most effective action you can take to ensure a clean, conclusive, and lender-acceptable outcome.

Reviewing the weed survey process in detail before your appointment will help you understand what surveyors expect and how findings are recorded. You can also consult a weed survey checklist to ensure nothing is overlooked before the visit. Being aware of potential property red flags associated with invasive weeds also helps you contextualise the surveyor’s findings within the broader conveyancing picture.

Pro Tip: Ask the surveyor to note any boundary areas they could not fully assess due to access issues. Lenders prefer transparent reports that acknowledge limitations over reports that appear to miss areas without explanation.

Interpreting results and ensuring lender approval

After the survey, interpreting the results clearly and knowing your next steps is critical for remortgage success. Survey reports can be dense documents, and understanding exactly what the findings mean for your application requires both technical and practical knowledge.

If the survey returns a clear result confirming no invasive weeds are present, your surveyor will issue a clean report. This document should be submitted directly to your lender or mortgage broker alongside your remortgage application. Most lenders will accept this without further conditions relating to invasive species.

Where Japanese Knotweed or another invasive species is identified, the report will classify the infestation by category and recommend a course of action. The key outcomes and corresponding steps are:

- Category 4 infestation (remote, low risk): Some lenders may still proceed with a management plan in place, even without a full IBG, though this is lender-dependent

- Category 3 infestation (within 7 metres of a structure): Most lenders will require an active management plan and an IBG before proceeding

- Category 2 or 1 infestation (close proximity to structures or causing damage): Lenders will typically require full remediation, ongoing treatment, and a long-term IBG of at least 5 years

- Inconclusive report: If the survey was conducted outside the growing season, lenders may request a follow-up assessment

Remediation options available to homeowners include:

- Thermo-electric treatment: A chemical-free method that delivers direct electrical energy into the rhizome network, depleting the plant’s internal energy reserves across multiple treatment sessions

- Root barrier installation: Physical barriers inserted into the soil to contain and prevent lateral rhizome spread

- Excavation: Full removal of contaminated soil and rhizome material, typically used where speed is essential or infestation is severe

- Herbicide treatment: A conventional chemical approach, though increasingly being replaced by eco-friendly alternatives

As lender policies vary considerably between strict approaches and those accepting an IBG, specialist lenders may be the most appropriate route for properties where remediation is underway but not yet complete. Understanding how to manage knotweed impact on your property value helps you frame the remediation investment not just as a lender requirement, but as a genuine long-term protection of your asset.

Presenting the outcome to your lender should always be done with a clear, organised summary: the survey report, the remediation specialist’s credentials, the IBG certificate where applicable, and a treatment timeline. Lenders respond well to evidence of proactive management and documented progress.

| Scenario | Lender likely response | Required documentation |

|---|---|---|

| No knotweed found | Proceed without weed-related conditions | Clean survey report |

| Knotweed found, Category 4 | May proceed with management plan | Survey report and management plan |

| Knotweed found, Category 2 or 3 | Retention or conditions applied | IBG, remediation plan, specialist report |

| Knotweed found, Category 1 | Possible refusal pending full remediation | All of the above plus treatment progress evidence |

The overlooked value of proactive weed checks

Now that you know the technical steps, consider why timing and proactive strategies are so often overlooked and why this oversight is genuinely costly. Most homeowners treat the weed survey as a box to tick once a lender requests it. That reactive approach is where the real expense begins.

The cost of a delayed remortgage, whether through a failed survey, a re-survey outside the growing season, or a scramble to secure an IBG under time pressure, can run to thousands in lost rate advantages, extended conveyancing fees, and bridging costs. Acting before the lender asks is not cautious; it is strategically sound.

There is also the question of knotweed industry impact on property values more broadly. Properties with unmanaged knotweed are valued lower, sell more slowly, and carry higher perceived risk. A proactive survey carried out during the May to September window, well ahead of a remortgage application, gives you time to respond to any findings without the pressure of a live application. It also gives you the opportunity to select a treatment method that aligns with your environmental values, rather than defaulting to the fastest or cheapest option under lender-imposed urgency. Proactive weed checks are not just procedural; they are a measurable investment in remortgage readiness.

Get expert support for your remortgage weed check

With your remortgage process prepared, here is where you can get specialist help for compliant weed checks.

Japanese Knotweed Agency delivers professional property surveys for invasive weeds across England, Wales, and Ireland, combining specialist plant identification expertise with formal documentation that meets lender requirements. As pioneers of chemical-free thermo-electric treatment, we also support homeowners through remediation, root barrier installation, and excavation works where required. Whether you are at the early preparation stage or already responding to a survey finding, our team can provide the expert guidance your remortgage demands. Explore our Japanese knotweed FAQ for answers to common lender queries, or review our weed survey process guide to understand exactly what to expect from a professional assessment.

Frequently asked questions

Do all lenders require a Japanese Knotweed survey for remortgaging?

No, not all lenders require one, but many have strict policies and may demand a survey report or an insurance-backed guarantee if knotweed is identified or suspected. Lender policies vary significantly, so confirming requirements with your specific lender before applying is always advisable.

When is the best time to have a weed check before remortgaging?

The growing season from May to September is optimal, as Japanese Knotweed is most visually identifiable during active growth and surveyors can produce conclusive, lender-acceptable reports during this window.

What happens if Japanese Knotweed is found during the survey?

Remediation and an insurance-backed guarantee are typically required before a lender will approve the remortgage. Lenders may demand IBG and documented treatment plans, and the urgency of action depends on the infestation category assigned in the survey report.

Can I use a specialist lender if standard lenders refuse my remortgage?

Yes, specialist lenders and bridging finance providers are often more flexible and can support remortgages where Japanese Knotweed remediation is active but incomplete, provided robust documentation is in place.