TL;DR:

- Most properties with Japanese knotweed can still obtain mortgages if professional surveys, management plans, and insurance-backed guarantees are in place. Lenders assess risk based on the RICS categories, with documentation from PCA-accredited contractors being essential for approval. Early detection, full disclosure, and verified treatment plans enable manageable mortgage processes despite knotweed presence.

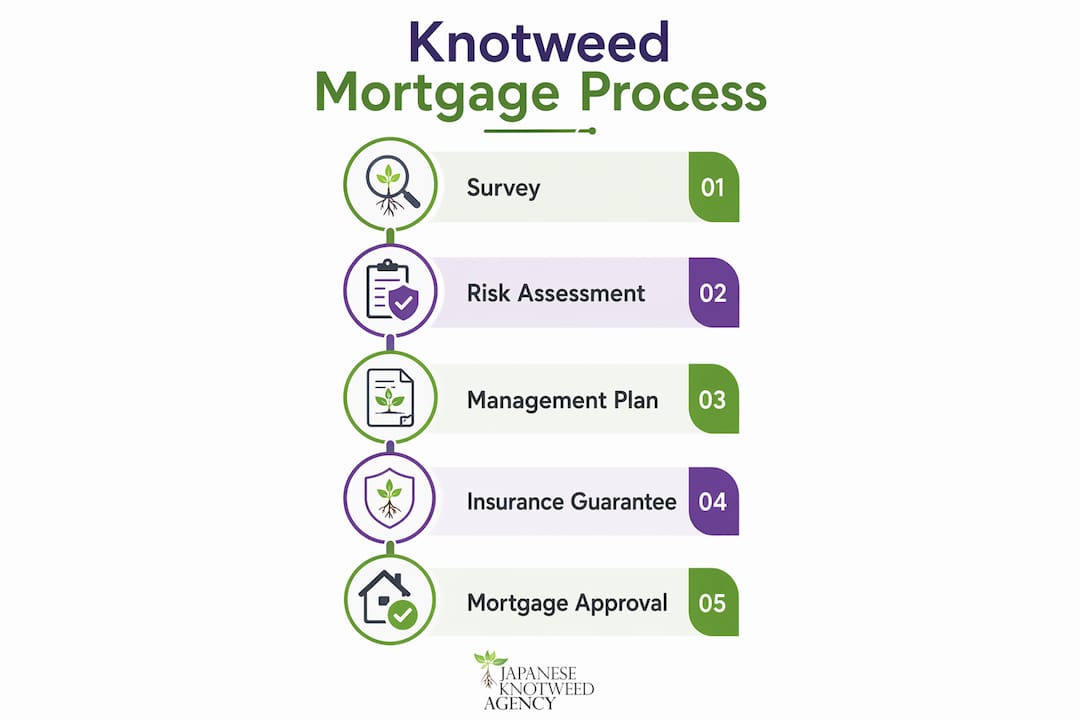

Knotweed mortgage issues arise when Japanese knotweed is identified on or near a property, triggering lender concerns about structural risk, long-term devaluation, and legal liability. The plant, formally classified as Fallopia japonica, can push through tarmac, concrete, and foundations, which explains why mortgage lenders treat its presence with considerable caution. The good news is that most properties with knotweed can still secure mortgage approval, provided the right professional documentation and treatment plans are in place. The RICS risk-based assessment framework, insurance-backed guarantees, and PCA-accredited management plans have transformed what was once an automatic refusal into a manageable, well-understood process.

What are the RICS risk categories for Japanese knotweed?

The RICS 2022 guidance replaced the old 7-metre rule with a four-category risk framework, labelled A through D, which lenders now use as the foundation for underwriting decisions. This shift means proximity alone no longer determines mortgage eligibility. Severity, structural impact, and the presence of a management plan all carry equal weight.

| RICS category | Description | Typical lender response |

|---|---|---|

| Category A | Knotweed present on neighbouring land, no encroachment | Mortgage usually proceeds without conditions |

| Category B | Knotweed within 7 metres of the property but no structural damage | Mortgage possible with management plan and IBG |

| Category C | Knotweed within the property boundary, no structural damage | Mortgage possible with active treatment and IBG |

| Category D | Knotweed causing or at risk of causing structural damage | Case-by-case underwriting; specialist report required |

Category B and C cases represent the majority of knotweed-affected transactions in England and Wales. In both scenarios, lenders will typically proceed once a PCA-accredited specialist has produced a management plan and an insurance-backed guarantee (IBG) is in place. Category D cases require more detailed structural assessments and are handled individually by lenders’ underwriting teams.

The specialist survey is the starting point for any categorisation. Without a formal RICS-compliant survey, no lender can assign a risk category, and the mortgage application stalls immediately. A qualified surveyor will assess the extent of the rhizome network, the distance from the structure, and any evidence of physical damage before producing a written report.

Pro Tip: Commission a specialist invasive weed survey before making a formal mortgage offer on any property where knotweed is suspected. Identifying the RICS category early prevents delays and gives you negotiating leverage on price.

How do management plans and guarantees enable mortgage approval?

A professional Japanese knotweed management plan is a documented programme of treatment, monitoring, and reporting produced by a PCA-accredited contractor. Management plans typically span three to five growing seasons, with treatment applied at key points in the plant’s annual growth cycle. The plan records each treatment visit, the methods used, and the observed response of the plant, creating an auditable trail that lenders can review.

The insurance-backed guarantee (IBG) is the document that gives lenders the confidence to proceed. An IBG is issued by an accredited provider and remains valid for between five and ten years, covering the property against knotweed resurgence during the guarantee period. If the original contractor ceases trading, the IBG remains enforceable through the insurer, which removes a significant lender concern about long-term risk.

PCA certification matters because lenders will not accept management plans from unaccredited contractors. The Property Care Association sets the professional standard for knotweed treatment in the UK, and its members are required to follow defined protocols for survey, treatment, and documentation. Submitting a plan from a non-PCA contractor is one of the most common reasons mortgage applications are delayed or declined at the documentation stage.

One detail that catches many buyers off guard: some lenders require evidence that at least the first treatment round has been completed before releasing mortgage funds, not merely that a plan exists. This means the seller, or the buyer in negotiation, may need to arrange and fund the initial treatment before exchange. Understanding this requirement early prevents last-minute delays at completion.

Professional knotweed management costs typically range from £950 to £4,000 depending on the scale and complexity of the infestation. This figure should be factored into any purchase negotiation, as it represents a direct cost to whoever commissions the treatment.

Pro Tip: Ask the seller to provide written confirmation of the PCA contractor’s accreditation number before accepting any existing management plan. Lenders will verify this independently, and an unaccredited plan will not satisfy their requirements.

What impact does knotweed have on property values and lending criteria?

Japanese knotweed can reduce property value by between 5% and 15%, depending on the severity of the infestation and whether a treatment plan is already in place. That reduction is not arbitrary. It reflects the cost of remediation, the perceived risk to the structure, and the reduced pool of buyers willing to proceed.

Buyer sentiment is a significant factor in this equation. Research shows that 33% of British adults refuse to purchase a property affected by knotweed, while 30% would consider buying if a treatment plan and a corresponding price reduction are offered. This means roughly a third of the potential market is removed from the outset, which directly affects the lender’s assessment of marketability and resale risk.

Lenders adjust their loan-to-value ratios on knotweed-affected properties to reflect this reduced marketability. A property that might ordinarily support a 90% LTV mortgage may be capped at 75% or 80% until treatment is underway or complete. This affects the deposit a buyer needs to provide and can make the purchase unviable without renegotiation.

The knotweed impact on property values is also relevant for remortgages and equity release. If knotweed is identified during a remortgage survey, the lender may reduce the available equity or impose conditions on the existing mortgage. Homeowners who discover knotweed during a remortgage application should engage a PCA-accredited specialist immediately rather than waiting for the lender to request documentation.

Home insurance is a related concern. Some insurers will exclude structural damage caused by knotweed if the plant was present and undisclosed at the time of taking out the policy. Reviewing your policy terms and disclosing knotweed presence to your insurer is a prudent step that sits alongside the mortgage process. For a detailed overview of this issue, the knotweed insurance guide from Japaneseknotweedagency covers the key considerations.

How can buyers and owners navigate knotweed mortgage issues effectively?

Dealing with knotweed in mortgages requires a structured approach from the moment the plant is identified. The steps below reflect the sequence that consistently produces the best outcomes for buyers, sellers, and existing homeowners.

-

Commission a specialist survey early. A RICS-compliant invasive weed survey establishes the risk category and gives all parties a factual basis for negotiation. Book a survey before making a formal offer where knotweed is visible or suspected.

-

Engage a PCA-accredited contractor. Only PCA-accredited specialists produce management plans and IBGs that lenders will accept. Verify accreditation before commissioning any work.

-

Work with a specialist mortgage broker. Lender flexibility on knotweed varies considerably. Some high-street lenders remain cautious, while specialist and challenger lenders apply more nuanced risk-based assessments. A broker with knotweed experience knows which lenders are most likely to approve a given category of case.

-

Disclose fully and document everything. Sellers have a legal obligation to disclose known knotweed presence on property information forms. Buyers who discover undisclosed knotweed after completion may have grounds for a legal claim, but prevention through transparency is far preferable to litigation.

-

Negotiate the purchase price to reflect remediation costs. If the seller has not commenced treatment, the buyer should seek a price reduction that covers the full cost of a management plan and IBG. This is standard practice and most sellers in this position expect it.

-

Confirm treatment commencement before exchange. Given that some lenders hold funds until the first treatment phase is complete, agreeing with the seller to commence treatment before exchange removes a potential completion risk.

Pro Tip: If you are selling a property with knotweed, commissioning a management plan before listing reduces the buyer pool impact and demonstrates good faith to both buyers and their lenders. It often results in a faster sale at a better price.

Key takeaways

Knotweed mortgage issues are manageable in the majority of cases when RICS risk categorisation, PCA-accredited management plans, and insurance-backed guarantees are in place from the outset.

| Point | Details |

|---|---|

| RICS categories replace the 7-metre rule | Categories A to D determine lender response; most cases in B and C can proceed with documentation. |

| IBGs are non-negotiable for lenders | Insurance-backed guarantees lasting 5 to 10 years give lenders the long-term assurance they require. |

| Property value reductions are real but recoverable | Knotweed can reduce value by 5% to 15%; active treatment plans reduce this impact significantly. |

| Treatment commencement matters as much as paperwork | Some lenders require the first treatment round to be complete before releasing mortgage funds. |

| Early specialist surveys prevent costly delays | A RICS-compliant survey before offer stage establishes the risk category and informs all negotiations. |

The unmortgageable myth: what experience actually shows

The claim that a knotweed-affected property is automatically unmortgageable is outdated and, frankly, damaging to property owners who deserve accurate information. Headlines stating knotweed properties are unmortgageable have persisted long after the industry moved on, and they cause unnecessary panic at what is already a stressful point in a property transaction.

What I have seen consistently is that the problems arise not from knotweed itself, but from incomplete paperwork, unaccredited contractors, and buyers or sellers who attempt to manage the process without specialist guidance. A Category C property with a properly documented management plan from a PCA-accredited contractor and a valid IBG is a mortgageable property. The lender’s concern is risk, and professional documentation addresses that risk directly.

The area where I would urge particular caution is the assumption that a management plan alone is sufficient. Thousands of mortgage applications on knotweed-affected properties succeed each year, but the ones that stall at the final stage often do so because the buyer assumed the plan was enough without confirming whether the lender required evidence of treatment commencement. That single oversight can delay completion by weeks.

The broader point is that lenders have become more sophisticated in their approach to knotweed risk, and that is a positive development. The shift to risk-based underwriting, guided by RICS categorisation, means that the system now rewards transparency and professional engagement rather than penalising every property where the plant appears. Work with accredited specialists, disclose everything, and engage a broker who understands the nuances. The process is manageable.

— Alan

How Japaneseknotweedagency supports mortgage compliance

Japaneseknotweedagency carries out professional invasive weed surveys across England, Wales, and Ireland, producing RICS-compliant reports that establish the risk category lenders require. Where treatment is needed, the team delivers thermo-electric treatment at up to 5,000 volts directly to the rhizome network, causing internal cell damage without the use of chemical herbicides. This chemical-free treatment approach achieves a 95% success rate and supports the documented management plans that satisfy lender requirements.

Root barrier installation and excavation works are also available for cases requiring physical containment or removal. Every survey and treatment programme is documented to the standard required for mortgage applications and insurance-backed guarantees. If you have identified knotweed on a property you are buying, selling, or remortgaging, book a survey with Japaneseknotweedagency to establish your risk category and understand your options. For answers to common questions about treatment and mortgage compliance, the Japaneseknotweedagency FAQ is a practical starting point.

FAQ

Does Japanese knotweed always prevent a mortgage?

Japanese knotweed does not automatically prevent mortgage approval. Most lenders will proceed in Categories A, B, and C when a PCA-accredited management plan and insurance-backed guarantee are in place.

What is an insurance-backed guarantee for knotweed?

An insurance-backed guarantee is a policy issued alongside a professional management plan, covering the property against knotweed resurgence for between five and ten years. Lenders require it as evidence of long-term risk management.

How much does a knotweed management plan cost?

Professional knotweed management plans typically cost between £950 and £4,000, depending on the size and severity of the infestation. This cost should be factored into purchase price negotiations.

Can other invasive plants cause mortgage problems?

Yes. Surveyors flagging invasive species beyond Japanese knotweed, including certain tree roots and other problematic plants, can trigger lender concerns and delay mortgage approvals.

Do I need a survey before making an offer on a knotweed property?

A specialist invasive weed survey before making a formal offer is strongly advisable. It establishes the RICS risk category, informs your negotiating position, and prevents delays once the mortgage application is submitted.